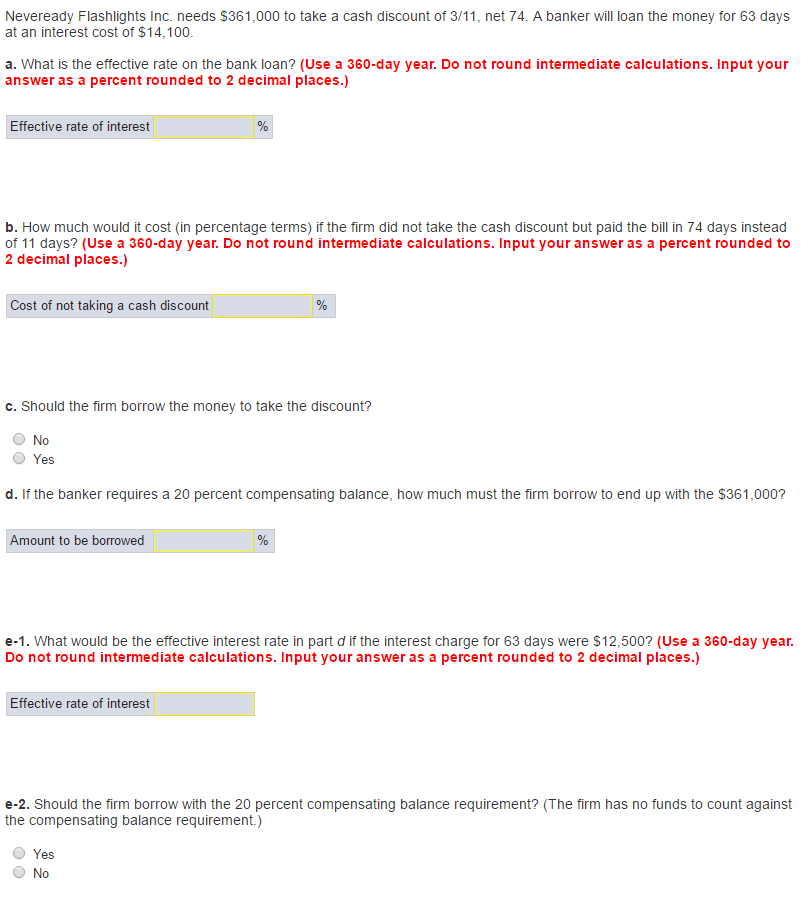

We consistently processes the pain and pledge of our state’s uprising getting racial fairness in the midst of a global fitness crisis. You can view our very own previous statements to the uprising right here, the COVID-19 webpage here, and you can our very own Competition & Housing capital cardiovascular system here. Expanding homeownership is a key component regarding racial security and you can wellness, thus all of our purpose is not more significant-and we’ll continue steadily to share new tales out of Habitat’s functions.

When you find yourself looking at purchasing your very first house, there’s a lot to take on. Not the very least ones will be monetary concerns, that go means not in the car or truck. Resident Innovation Manager Pa Lor teaches you a few of them during the the latest movies answering popular questions regarding homeownership.

- How lenders make use of income to check your financial maturity [0:50]

- The necessity of with coupons before applying having home financing [1:15]

- How do your borrowing feeling your ability to locate a mortgage? [1:53]

- What’s the debt ratio, as well as how big be it? [2:26]

- What character does your credit history enjoy on the financial readiness? [3:46]

- Are you currently psychologically and you may emotionally happy to get a house? [5:04]

“When you’re buying a home, I think the main thing is to make sure you’re comparing and you can planning economically,” states Pa. These represent the primary standards you can utilize to arrange order your earliest house.

Regarding the movies, Pa shows you the idea of mortgage maturity, that can help you plan out your money prior to purchasing your first home. Here you will find the fundamental elements of home loan maturity.

Earnings – Your income would-be one of the first something a lender discusses after you make an application for home financing. “This might be going to be your greatest resource,” Pa says. “Your revenue would be what is regularly meet the requirements your for a loan installment loans Louisiane, and has now to get proven, stable, and you will continuing.”

Coupons – And additionally their normal money, you should generate some sort of discounts before buying a good house. You are probably planning dip in it to invest review charges, closing costs, or maybe even a down-payment for the family.

Credit – Borrowing is really what identifies although you’ll be approved to have a loan. Appropriate credit ratings are different of the financing and you will vendor, however, Pa states one to “extremely financial institutions will need a beneficial 640 or higher.”

Obligations Proportion – Your debt ratio try a measurement regarding how much cash you will be making versus exactly how much from it has been invested to invest down loans. About video, Pa claims, “From the mortgage industry, your entire expense [combined],” including the home loan you are trying to get, “shouldn’t be more 43 percent of your income.”

Eg, Dual Metropolises Habitat angles their month-to-month mortgage repayment to your from the 30 percent of your own earnings, which means that your own kept loans repayments can’t go beyond thirteen % from your earnings when you need to getting acknowledged for a financial loan (for all in all, 43%). “When you yourself have lots of current the debt which have fund, college loans, credit cards, just what maybe you’ve, just make sure that you are benefiting from of those things reduced out-of upfront you to procedure,” Pa claims.

Credit rating – Bankruptcy, judgments, and you will series normally echo negatively on your credit score and you can feeling what you can do discover a home loan. “If you have got a current case of bankruptcy, it may take sometime about how to run reconstructing borrowing from the bank before you can be considered so you can borrow cash buying a house,” Pa explains. “An abundance of loan providers requires which you pay those individuals judgments and you will series off one which just pick a property.”

Affordability

Together with your mortgage maturity, believe carefully the expense you can sustain when buying a property. Pa claims you should “guarantee that the funds is there” before you decide on home to your own goals. “So what can you pay for? What’s property rate that you are comfortable with? What exactly is a monthly payment that you will be comfortable with?”

Currency isn’t the simply grounds to take on when buying a property. “To purchase a property is very much mental and you will mental also due to the fact monetary,” Pa says. “While the a resident, you’ll have to make family solutions. You will need to be ready to enhance one thing, or spend people to look after the things. Are you presently mentally happy to do the things? Isn’t it time and you may willing to discover? Could you spade [your own driveway] and to mow your own turf? All of those everything is something that you have to inquire oneself.”

Info to evaluate their financial readiness

When you yourself have questions regarding the financial readiness otherwise tips raise your chances of being qualified, you’ll find locations to check out score let. “There’s a lot of information available to choose from to help you purchase the first household,” Pa states.

That have local monetary sessions and you will homeownership pros, Dual Towns Habitat is among the most all of them. We will let determine your home loan maturity and get ways to get your money able when you decide order your basic house.

For people who discovered so it video beneficial, listed below are some alot more tips for earliest-big date homebuyers on Twin Metropolises Environment for Humankind YouTube station!

Leave a Reply